You’re experiencing severe chest pain at 2 AM in Manhattan. Your first thought should be getting help, not worrying about the bill. But let’s be honest—the emergency room cost in New York is a legitimate concern that keeps many residents anxious about seeking urgent medical care.

Here’s what you need to know right now: The average emergency room cost in New York ranges from $600 to $3,000 for non-life-threatening conditions, but this number tells only part of the story. Your actual bill depends on your insurance status, which hospital you visit, the severity of your condition, and whether you know how to navigate New York’s complex healthcare billing system.

This comprehensive guide walks you through everything New York residents need to know about ER costs in 2026. You’ll learn exact prices at major New York hospitals, how to use your insurance effectively, when urgent care makes more financial sense, and most importantly—how to dramatically reduce or even eliminate your ER bill through programs most New Yorkers don’t know exist.

By the time you finish reading, you’ll understand your rights as a patient, know which financial assistance programs can help you, and have actionable strategies to avoid overpaying for emergency care. Your health matters more than any bill, but you deserve to know what you’re facing and how to handle it.

Table of Contents

How Much Does an ER Visit Cost in New York?

Let’s start with the numbers you actually need. The emergency room cost in New York varies significantly, but understanding the ranges helps you prepare financially and make informed decisions about where to seek care.

New York State averages $1,668 per ER visit, placing it as the 22nd most expensive state in the nation according to the most recent comprehensive state-by-state analysis. However, this average masks substantial regional variation between New York City and upstate areas, as well as differences between hospital systems.

Here’s what you’ll typically pay based on your insurance status:

| Insurance Status | Typical Cost Range | What You Actually Pay |

|---|---|---|

| With insurance (after deductible met) | $100-$500 copay | Just your copay amount |

| With insurance (before deductible) | Full cost until deductible met | $600-$3,000+ until deductible satisfied |

| Without insurance (self-pay) | $600-$3,000+ | Full amount, but negotiable |

| Critical/complex cases | $5,000-$20,000+ | Varies by insurance/assistance programs |

National context matters: While the national average for an ER visit sits between $1,500 and $3,000, New York falls in the middle range. You’ll pay significantly more than residents of Maryland (average $623) or Maine (average $952), but considerably less than patients in Florida (average $3,102) or New Jersey (average $3,087).

The reality for uninsured New Yorkers: Without insurance, you’re looking at $600-$3,000 for straightforward visits like treating a sprained ankle, minor cuts requiring stitches, or UTIs. More complex situations involving extensive testing, imaging, or specialist consultations can easily reach $5,000-$10,000. Life-threatening emergencies requiring surgery or intensive care can exceed $20,000.

The insurance advantage: With insurance, your out-of-pocket responsibility typically consists of your copay ($100-$500 for most plans) plus any deductible you haven’t met yet. Many insurance plans waive the copay if you’re admitted to the hospital, and under the Affordable Care Act, your maximum out-of-pocket expenses for the year are capped at $9,450 for individuals and $18,900 for families in 2026.

Understanding these baseline numbers helps you evaluate whether alternative care options like urgent care make financial sense for your situation—a topic we’ll explore in detail later in this guide.

What Determines Your Emergency Room Bill in New York

The emergency room cost in New York isn’t a fixed number. Multiple factors influence what you’ll ultimately pay, and understanding these variables empowers you to ask better questions and potentially reduce your expenses.

Facility Type Makes a Massive Difference

Not all emergency rooms charge the same rates. The type of facility you visit significantly impacts your final bill.

Hospital-based emergency departments represent the traditional ER model. These are emergency departments physically located within hospitals like Mount Sinai, NYU Langone, or NYC Health + Hospitals facilities. They generally charge standard emergency room rates.

Freestanding emergency departments look and feel like regular ERs but aren’t attached to hospitals. While convenient, they typically charge 50% more than hospital-based ERs for similar services. If you have a choice, hospital-based facilities usually cost less.

Teaching hospitals versus community hospitals also show pricing variations. Major academic medical centers in New York City (Columbia, NYU, Cornell) often charge premium rates reflecting their advanced capabilities and specialist availability. Smaller community hospitals, particularly upstate, generally have lower baseline charges.

Public versus private hospital systems: NYC Health + Hospitals, the city’s public hospital system, typically offers more affordable rates and more generous financial assistance programs compared to private hospital networks.

Level of Care Required

Emergency departments use the Emergency Severity Index (ESI) to classify patients from Level 1 (most critical) to Level 5 (least urgent). This classification directly determines your facility fee—the base charge just for walking through the ER doors.

| Severity Level | Description | Facility Fee Range (NY) | Typical Examples |

|---|---|---|---|

| Level 1 | Life-threatening, immediate care needed | $1,200-$4,500 | Cardiac arrest, severe trauma, stroke |

| Level 2 | Emergency, potentially life-threatening | $900-$2,500 | Chest pain, severe breathing difficulty |

| Level 3 | Urgent, not immediately life-threatening (most common) | $700-$1,500 | Moderate pain, broken bones, lacerations |

| Level 4 | Semi-urgent, stable condition | $400-$900 | Minor injuries, mild infections |

| Level 5 | Non-urgent, can be delayed | $250-$600 | Prescription refills, minor complaints |

The vast majority of ER visits—approximately 60%—fall into Level 3. Understanding this classification helps you anticipate costs and also explains why seemingly similar conditions might generate different bills based on how the triage nurse assesses your initial presentation.

Additional Services and Tests

Beyond the facility fee, every diagnostic test, medication, and supply adds to your bill. These charges accumulate quickly:

Laboratory work:

- Basic blood work (CBC, metabolic panel): $100-$300

- Comprehensive testing panels: $300-$500

- Specialized tests (cardiac enzymes, toxicology): $200-$400

Imaging studies:

- X-rays (single view): $200-$400

- X-rays (multiple views): $400-$600

- CT scans: $500-$3,000

- MRI: $1,000-$5,000

- Ultrasound: $300-$1,000

Medications and treatments:

- IV fluids and administration: $100-$400

- Injectable medications: $50-$300 per dose

- Oral medications: $20-$100

- IV antibiotics: $200-$500

Medical supplies:

- Splints and braces: $50-$300

- Casting materials: $100-$500

- Suture kits and wound closure: $100-$400

- Bandages and dressings: $20-$150

A patient visiting the ER with abdominal pain might receive a basic exam (facility fee), blood work ($300), CT scan ($1,500), IV fluids ($200), and pain medication ($100), totaling over $2,800 before insurance.

Time of Visit

Evening, overnight, and weekend visits often incur higher charges due to staffing differentials and premium pay requirements. While you shouldn’t delay emergency care to save money, understanding this factor explains some billing variations.

Hospital Location

Geography significantly impacts the emergency room cost in New York. Manhattan hospitals typically charge 20-40% more than similar facilities in the Bronx, Queens, or Staten Island. Upstate New York hospitals generally charge 20-30% less than New York City facilities across the board.

This regional variation reflects differences in operating costs, local wage standards, and market competition rather than quality of care.

Length of Stay

Time spent in the emergency department affects your bill. A quick two-hour visit for stitches costs considerably less than an eight-hour stay for observation and multiple rounds of testing. If you’re placed in “observation status” (not quite admitted but not discharged), expect higher charges for extended facility use.

ER Costs at Major New York Hospitals (2026)

The emergency room cost in New York varies substantially between hospital systems. While exact prices depend on your specific condition and treatment, understanding general cost ranges at major facilities helps you make informed decisions.

Important note: Federal law requires that you receive emergency care regardless of which hospital you visit or whether it’s in your insurance network. However, knowing typical pricing helps with financial planning and post-visit bill management.

NYC Health + Hospitals (Public System)

New York City’s public hospital network operates 11 acute care hospitals across the five boroughs, including Bellevue, Elmhurst, Harlem Hospital, Kings County, Jacobi, Coney Island, and Lincoln.

Estimated cost range: $600-$2,000 for typical ER visits

Key advantages:

- Generally lower baseline charges than private hospitals

- Most generous financial assistance programs in NYC

- “Options” program for uninsured patients

- Sliding scale fees based on income

- No one turned away for inability to pay

- Multilingual services standard

Best for: Uninsured patients, low-income residents, those needing financial assistance

NYC Health + Hospitals facilities have explicit policies to help New Yorkers access care regardless of immigration status or ability to pay. If you’re uninsured or underinsured, starting here often results in significantly lower out-of-pocket costs.

Mount Sinai Health System

Mount Sinai operates multiple emergency departments across Manhattan, Queens, Brooklyn, and Long Island, including Mount Sinai Hospital, Mount Sinai West, Mount Sinai Beth Israel, and Mount Sinai Queens.

Estimated cost range: $1,200-$3,000+ for typical ER visits

Characteristics:

- Advanced tertiary care capabilities

- Specialized emergency services (cardiac, pediatric, trauma)

- Prices vary by specific campus

- Robust financial assistance program available

- Major teaching hospital with latest technology

Mount Sinai’s flagship Manhattan locations typically charge at the higher end of this range, while outer borough facilities may be slightly lower.

NYU Langone Health

NYU Langone operates emergency departments in Manhattan (Tisch Hospital, Kimmel Pavilion) and Brooklyn (NYU Langone Hospital—Brooklyn), plus specialized pediatric emergency services.

Estimated cost range: $1,500-$3,500+ for typical ER visits

Characteristics:

- Premium pricing reflecting advanced capabilities

- Nationally ranked specialties

- State-of-the-art facilities

- Comprehensive financial counseling available

- Known for shorter wait times at some locations

NYU Langone facilities rank among New York’s more expensive options, but they offer cutting-edge diagnostic capabilities and specialist availability 24/7.

NewYork-Presbyterian Hospital

NewYork-Presbyterian’s massive network includes Columbia campus, Weill Cornell campus, and multiple community hospitals throughout the New York metro area.

Estimated cost range: $1,400-$3,200+ for typical ER visits

Characteristics:

- One of the nation’s largest hospital systems

- High patient volume ERs

- Academic medical center pricing

- Excellent specialist access

- Financial assistance programs available

The specific campus significantly affects pricing, with Manhattan locations generally charging more than Westchester County facilities.

Northwell Health (Long Island/Queens)

Northwell Health, New York’s largest health system, operates 23 hospitals including Long Island Jewish Medical Center, North Shore University Hospital, Lenox Hill Hospital, and multiple facilities across Long Island and Queens.

Estimated cost range: $1,100-$2,800 for typical ER visits

Characteristics:

- Wide geographic coverage

- Range of facility types from community to tertiary care

- Generally competitive pricing

- Strong community hospital network

- Comprehensive financial assistance policies

Northwell facilities in Queens and Long Island often provide slightly lower costs than comparable Manhattan hospitals while maintaining high-quality emergency care.

Upstate New York Hospitals

Major upstate emergency departments include University Hospital (Syracuse), Strong Memorial Hospital (Rochester), Albany Medical Center, and Buffalo General Medical Center.

Estimated cost range: $800-$2,200 for typical ER visits

Key differences:

- 20-30% lower than NYC on average

- Reflect lower regional operating costs

- Equally capable emergency care

- Less congestion, often shorter wait times

- Financial assistance programs widely available

If you live upstate, you’ll generally face lower baseline emergency room costs than New York City residents, though the same factors (severity, tests, treatments) still apply.

How to Find Specific Hospital Prices

New York hospitals are legally required to post their “chargemaster” prices online. Here’s how to access them:

- Visit the hospital’s website

- Look for “Price Transparency,” “Standard Charges,” or “Price Estimator” links (usually in footer)

- Search for CPT codes 99281-99285 (emergency department visit levels)

- Download their machine-readable file for detailed pricing

Reality check: Chargemaster prices represent the hospital’s list prices before insurance negotiations or financial assistance. Almost no one pays these full amounts. They serve as a starting point for understanding relative costs between facilities rather than what you’ll actually owe.

What You’ll Pay for Common ER Visits in New York

Understanding condition-specific costs helps you anticipate expenses and evaluate whether urgent care might be a more cost-effective alternative for non-emergencies. Here’s what New Yorkers typically pay for common emergency room visits.

| Condition/Reason for Visit | Without Insurance (NY Estimate) | With Insurance (Typical Copay) | Urgent Care Alternative Cost |

|---|---|---|---|

| Minor cut requiring stitches | $600-$1,800 | $100-$300 | $150-$350 ✓ |

| Sprained ankle or wrist | $800-$2,000 | $100-$350 | $125-$300 ✓ |

| Mild allergic reaction | $500-$1,500 | $100-$300 | $100-$200 ✓ |

| Urinary tract infection (UTI) | $900-$2,500 | $150-$400 | $100-$250 ✓ |

| Migraine headache | $700-$2,000 | $100-$350 | $125-$275 ✓ |

| Minor burns (1st or 2nd degree) | $600-$1,800 | $100-$350 | $150-$300 ✓ |

| Flu or high fever | $700-$2,000 | $100-$300 | $100-$200 ✓ |

| Ear infection | $600-$1,500 | $100-$300 | $100-$200 ✓ |

| Minor asthma attack | $900-$2,500 | $150-$400 | $150-$350 ✓ |

| Chest pain (ruled out cardiac) | $1,500-$4,000 | $200-$500 | Not appropriate ✗ |

| Broken bone (no surgery needed) | $1,200-$3,500 | $200-$500 | Not appropriate ✗ |

| Severe abdominal pain | $1,500-$4,500 | $200-$500 | Not appropriate ✗ |

| Deep laceration/severe bleeding | $1,000-$3,000 | $150-$500 | Not appropriate ✗ |

| Broken bone requiring surgery | $10,000-$30,000+ | $500-$3,000+ (deductible/coinsurance) | Not appropriate ✗ |

| Heart attack | $15,000-$50,000+ | $1,000-$5,000+ (varies widely) | Not appropriate ✗ |

Why such wide ranges? Several factors explain the cost variation:

Diagnostic testing drives costs: A patient with chest pain might receive basic monitoring and be discharged ($1,500), or undergo extensive cardiac enzyme testing, EKG, chest X-ray, and CT scan ($4,000+). The presenting symptoms are similar, but the diagnostic pathway dramatically affects the final bill.

If you’ve experienced chest pain that turned out to be non-cardiac, working with a fitness professional and getting baseline cardiovascular assessments like VO2 max testing can help you understand your heart health and avoid future ER visits.

NYC premium: New York City hospitals typically charge 25-40% more than upstate facilities for identical conditions. A UTI treated in Buffalo might cost $900, while the same treatment at a Manhattan ER could reach $2,500.

Hospital variation: Even within NYC, public hospitals (NYC Health + Hospitals) generally charge less than private academic medical centers for comparable care.

Insurance negotiation: The “without insurance” prices shown represent what hospitals bill self-pay patients. However, these are negotiable, and financial assistance programs can reduce them by 50-100% for eligible patients.

Real Cost Examples from New York Patients

Case 1: Sprained ankle in Manhattan

- Hospital: Private academic medical center

- Services: ER visit, X-ray (2 views), splint, crutches

- Billed charges: $2,847

- With insurance (after copay): $250

- Self-pay negotiated: $1,200 (58% discount)

Case 2: Child with high fever in Queens

- Hospital: Community hospital

- Services: ER visit, rapid flu test, throat culture, oral medication

- Billed charges: $1,456

- Medicaid patient: $0

- Without insurance (before assistance): $1,456

Case 3: Chest pain (false alarm) in Brooklyn

- Hospital: Large health system

- Services: ER visit Level 2, EKG, chest X-ray, cardiac enzymes, 4-hour observation

- Billed charges: $5,234

- With insurance (after deductible): $500 copay + $1,047 coinsurance = $1,547

- Self-pay with financial assistance: $0 (100% charity care)

These real examples illustrate how the same condition can generate vastly different patient responsibility based on insurance status, hospital choice, and knowledge of financial assistance programs.

When the Same Condition Costs Dramatically Different Amounts

Consider two New York patients with identical UTIs:

Patient A: Goes to urgent care in the Bronx

- Visit fee: $175

- Urinalysis: $30

- Antibiotic prescription: $15

- Total: $220

- Time: 45 minutes

Patient B: Goes to Manhattan ER

- ER facility fee (Level 3): $1,200

- Physician fee: $450

- Urinalysis: $125

- Additional blood work: $275

- IV fluids: $200

- IV antibiotics: $300

- Prescription: $40

- Total: $2,590

- Time: 4 hours

Both patients receive effective treatment, but Patient B pays nearly 12 times more and waits five times longer. Understanding when urgent care suffices can save you thousands of dollars—a topic we’ll cover in detail shortly.

How Insurance Affects Emergency Room Costs in New York

Your insurance status fundamentally changes the emergency room cost in New York. Understanding how different insurance types handle ER visits helps you anticipate expenses and use your coverage effectively.

Medicaid (New York State Medicaid)

New York’s Medicaid program provides the most comprehensive ER coverage with minimal patient cost.

ER copay: $0 for most enrollees Coverage includes:

- All medically necessary emergency services

- Ambulance transportation

- All diagnostic tests and imaging

- Medications administered in the ER

- Follow-up care related to the emergency

Who qualifies:

- Income limits vary by household size and category

- Pregnant women qualify at higher income thresholds

- Children eligible through Child Health Plus

- Elderly and disabled individuals under specific programs

Emergency Medicaid: Even if you don’t qualify for regular Medicaid, Emergency Medicaid covers emergency services regardless of immigration status. You can apply at the hospital or local Medicaid office, and coverage applies retroactively to the date of service.

Medicare (Original Medicare Parts A & B)

Medicare beneficiaries face different cost structures depending on whether they’re admitted to the hospital.

If treated and released:

- Part B covers ER services

- You pay 20% of Medicare-approved amount after Part B deductible ($240 in 2026)

- Example: Medicare-approved amount is $1,500. You pay $240 deductible + $252 (20% of $1,260) = $492

If admitted to hospital:

- Part A hospital insurance applies

- You pay $1,632 deductible per benefit period (2026 amount)

- ER copay typically waived when admitted

Medicare Advantage plans:

- Copays typically $50-$350 for ER visits

- Often waived if admitted within 24 hours

- Out-of-pocket maximums apply (varies by plan, typically $3,000-$8,000 annually)

Commercial Insurance (Private Plans)

Most employed New Yorkers have commercial insurance through employers. Major carriers in New York include Empire BlueCross BlueShield, Healthfirst, Oscar Health, Emblem Health, Fidelis Care, United Healthcare, and Aetna.

Typical ER copay structure:

- Standard copay: $100-$500 per ER visit

- High-deductible plans: You pay full cost until deductible met, then copay applies

- Many plans waive copay if admitted to hospital

How deductibles work: If you haven’t met your annual deductible, you typically pay the full negotiated rate (not the chargemaster price) until your deductible is satisfied.

Example with $2,000 deductible:

- ER visit costs $3,000 (hospital’s charge)

- Insurance negotiated rate: $1,800

- You’ve paid $500 toward deductible this year

- You pay: $1,500 (remaining deductible) + copay if applicable

- Insurance pays: $300

After deductible is met:

- You pay only your copay ($150-$500 typically)

- Insurance pays the rest

Out-of-pocket maximum protection: Under the Affordable Care Act, your maximum annual out-of-pocket costs are capped at $9,450 for individuals and $18,900 for families in 2026. Once you hit this limit, insurance pays 100% of covered services for the rest of the year.

In-Network vs. Out-of-Network: Critical Protection for ER Visits

Here’s extremely important news for New York residents: You cannot be balance-billed for emergency services, even at out-of-network hospitals.

Under the No Surprises Act (federal law, effective January 2022):

- Emergency services must be covered at in-network cost-sharing rates

- Applies even if you go to an out-of-network hospital

- Protects you from surprise bills for out-of-network ER doctors

- You pay only your in-network copay/coinsurance/deductible

New York’s additional protections:

- NY had surprise billing protections before the federal law

- Provides even stronger consumer safeguards in some situations

- Independent Dispute Resolution (IDR) process available

- Limits your financial responsibility to in-network amounts

What this means practically: If you have a medical emergency in Manhattan but the nearest hospital is out-of-network for your insurance, you’ll pay the same copay as if you’d gone to an in-network facility. The hospital and your insurance company resolve payment disputes through arbitration—you’re protected from the difference.

Important exception: These protections apply only to emergency services. If you’re admitted and receive non-emergency follow-up care or elective procedures at an out-of-network hospital, different rules apply.

What Insurance Typically Covers in the ER

Always covered for emergencies:

- Medical screening examination

- Emergency physician services

- Facility fees

- Diagnostic tests necessary for emergency care

- Emergency medications and treatments

- Medical supplies used during emergency care

May have limitations:

- Ambulance transportation (often separate copay/deductible)

- Non-emergency follow-up care

- Elective procedures performed during ER visit

- Experimental or investigational treatments

- Cosmetic procedures

The Surprise Billing Problem (and New York’s Solution)

Before 2022, many New York patients faced shocking bills when out-of-network doctors treated them in in-network ERs. A common scenario: You go to an in-network hospital for chest pain, but the emergency physician, radiologist, or specialist who treats you is out-of-network. You’d receive separate bills for thousands of dollars beyond your copay.

New York solved this problem:

State protections (2014-present):

- Banned balance billing for emergency services

- Established Independent Dispute Resolution for billing disputes

- Protected consumers from unexpected charges

Federal No Surprises Act (2022-present):

- Extended similar protections nationwide

- Strengthened consumer safeguards

- Created uniform federal standards

Your rights:

- You cannot be asked to waive your protections, even if you sign forms

- Your consent is not required for these protections to apply

- Out-of-network providers cannot bill you more than in-network cost-sharing

- Disputes between providers and insurers don’t involve you

If you receive a surprise bill:

- Contact your insurance company immediately

- File a complaint with the New York State Department of Financial Services (1-800-342-3736)

- Don’t pay disputed amounts

- Request Independent Dispute Resolution if needed

New York’s protections mean you can focus on getting emergency care without fear of financial ambush from out-of-network billing.

Emergency Room Costs for Uninsured New Yorkers

Lacking health insurance doesn’t mean you’ll face the full emergency room cost in New York without help. Multiple programs, laws, and negotiation strategies can dramatically reduce your financial burden.

What to Expect as an Uninsured Patient

You will receive care: Federal EMTALA (Emergency Medical Treatment and Labor Act) law requires every ER to provide medical screening and stabilizing treatment regardless of your ability to pay. Immigration status, employment status, and financial resources don’t affect your right to emergency care.

Initial billing: Hospitals typically bill uninsured patients their “chargemaster” rates—the list prices before insurance discounts. These are often 2-3 times higher than what insurance companies pay for identical services.

Average costs for uninsured New Yorkers:

- Simple ER visits (Level 3-4): $600-$2,000

- Moderate complexity (Level 2-3): $1,500-$4,000

- High complexity or observation (Level 1-2): $3,000-$10,000

- Critical care with admission: $10,000-$50,000+

The good news: These billed amounts are rarely what you’ll actually pay if you know how to navigate the system.

Self-Pay Discounts

Many New York hospitals offer “prompt pay” or “self-pay” discounts ranging from 20% to 50% off chargemaster prices if you pay within a specified timeframe (typically 30-90 days).

How to request:

- When registering at the ER, inform staff you’re self-pay

- Ask to speak with a financial counselor before or immediately after treatment

- Specifically request: “What self-pay discounts do you offer?”

- Ask for the discount in writing

- Negotiate the discount percentage if possible

Example:

- ER bill: $3,200

- 40% self-pay discount if paid within 30 days: -$1,280

- Your cost: $1,920

- Additional 15% discount if paid in full immediately: -$288

- Final cost: $1,632

Some hospitals extend better discounts for immediate payment. If you have savings or access to low-interest credit, this strategy can save substantially.

New York’s Financial Assistance Law (FAL)

This is the most powerful tool for uninsured and underinsured New Yorkers. New York State law requires non-profit hospitals to provide financial assistance to eligible low-income patients.

Key provisions:

- Applies to patients with household income up to 300% of federal poverty level (varies by hospital)

- Can reduce your bill by 75% to 100%

- Retroactive applications accepted up to 2 years after service

- Hospitals must screen patients and provide applications

- Credit reporting prohibited while application is pending (up to 2 years)

2026 Income eligibility (approximate—hospitals vary):

- Individual: Up to ~$45,000/year may qualify for full or partial assistance

- Family of 2: Up to ~$60,000/year

- Family of 4: Up to ~$93,000/year

Typical discount tiers:

- 0-150% FPL: 100% discount (free care)

- 150-200% FPL: 75% discount

- 200-250% FPL: 50% discount

- 250-300% FPL: 25% discount

What you need to apply:

- Proof of income (pay stubs, tax returns, benefit letters)

- Proof of residency in New York

- Household size documentation

- Bank statements (sometimes)

- Application form (available from hospital financial counseling department)

How to apply:

- Contact the hospital’s financial counseling department

- Request a financial assistance application

- Submit documentation promptly

- Follow up weekly on application status

- Appeal if denied

Critical timing: You can apply for financial assistance up to 2 years after your ER visit. Even if you’ve already received bills or been contacted by collections, you can still apply and qualify retroactively.

Charity Care Programs at Major New York Hospitals

Beyond state-mandated financial assistance, many hospitals operate charity care programs with even more generous terms.

NYC Health + Hospitals:

- Most generous financial assistance in New York City

- “Options” program for uninsured patients

- Sliding scale fees based on income

- Many services free for patients under 200% FPL

- No citizenship or immigration status requirements

- Application assistance available in multiple languages

Major private systems:

- Mount Sinai: Financial assistance up to 400% FPL for some services

- NYU Langone: Charity care and payment plans

- NewYork-Presbyterian: Financial Assistance Program with sliding scale

- Northwell Health: Comprehensive financial assistance policies

What charity care typically covers:

- Emergency department services

- Inpatient hospital care

- Outpatient procedures

- Necessary follow-up care

Real example: An uninsured patient in Queens received a $7,800 ER bill for abdominal pain requiring CT scan and observation. Household income: $38,000 (single person). Applied for charity care at the NYC Health + Hospitals facility. Result: 100% discount, $0 final bill.

Emergency Medicaid in New York

Even if you don’t qualify for regular Medicaid, Emergency Medicaid covers emergency services for anyone who:

- Meets Medicaid income requirements

- Requires emergency medical care

- Is ineligible for regular Medicaid only due to immigration status

Who qualifies:

- Undocumented immigrants

- Visitors to the U.S.

- Others ineligible for regular Medicaid due to immigration status

What it covers:

- Emergency room services

- Emergency surgery

- Dialysis

- Labor and delivery

- Other emergency medical conditions

How to apply:

- Apply at the hospital or local Department of Social Services

- Bring identification and proof of income

- Coverage applies retroactively to date of service

- No citizenship or immigration questions affect emergency care

Important protection: New York has sanctuary policies protecting immigrants seeking healthcare. Your immigration status information will not be shared with federal immigration authorities when you seek emergency care.

Payment Plans: Making ER Bills Manageable

If you don’t qualify for full financial assistance, most New York hospitals offer interest-free payment plans making large bills manageable over time.

Typical payment plan terms:

- $25-$100 minimum monthly payment

- 12-24 month standard plans

- Extended plans (36-48 months) for larger balances

- No interest or fees if you maintain payments

- No credit check required

How to set up:

- Contact hospital billing department before due date

- Propose monthly payment you can afford

- Get agreement in writing

- Set up automatic payments to avoid missed payments

- Keep records of all payments

Avoiding collections: As long as you maintain regular payments—even small amounts—hospitals typically don’t send accounts to collections. A $5,000 ER bill paid at $100/month over 50 months is better than damaging your credit with unpaid debt.

What NOT to Do as an Uninsured Patient

Don’t ignore bills: This leads to collections, credit damage, and potential lawsuits. Even if you can’t pay, communicate with the hospital.

Don’t pay immediately without investigating options: Take time to apply for financial assistance, request itemized bills, and negotiate.

Don’t assume you don’t qualify for help: Income limits are higher than most people expect. Always apply.

Don’t use high-interest credit cards without exploring all options first: Paying 18-24% interest on medical debt should be your last resort after exhausting financial assistance, charity care, and payment plans.

Don’t avoid future emergency care due to outstanding bills: Your health matters more than debt. Hospitals must treat emergencies regardless of past balances.

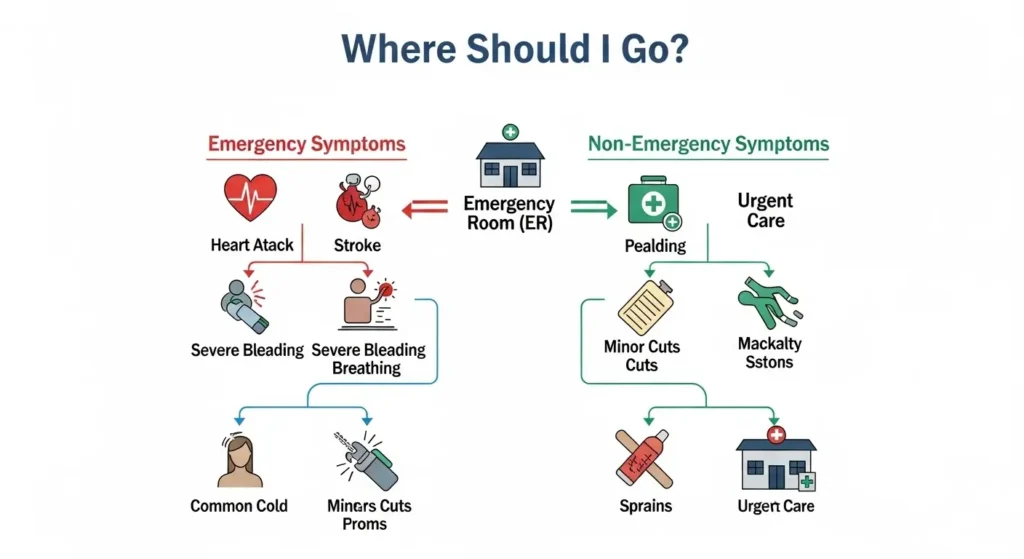

ER vs. Urgent Care: Making the Smart Financial Choice

Understanding when to choose urgent care over an emergency room can save New York residents $500 to $2,500 per visit. Here’s how to make the right decision for both your health and your wallet.

Cost Comparison: The Numbers That Matter

| Care Setting | Average Cost NY | Wait Time | Hours of Operation | Capabilities |

|---|---|---|---|---|

| Emergency Room | $600-$3,000+ | 2-6 hours | 24/7/365 | Full diagnostic, life-threatening emergencies |

| Urgent Care | $100-$250 | 15-60 minutes | Extended hours, 7 days/week (typically 8am-8pm) | Basic diagnostics, non-life-threatening |

| Primary Care | $100-$200 | Scheduled appointment | Business Hours | Preventive care, chronic conditions |

| Telehealth | $40-$75 | Immediate-30 min | 24/7 (varies by provider) | Consultation, simple diagnoses |

Real savings examples:

UTI treatment:

- ER cost: $900-$2,500

- Urgent care cost: $100-$250

- Savings: $800-$2,250

Sprained ankle:

- ER cost: $800-$2,000

- Urgent care cost: $125-$300

- Savings: $675-$1,700

Minor cut requiring stitches:

- ER cost: $600-$1,800

- Urgent care cost: $150-$350

- Savings: $450-$1,450

When You MUST Go to the ER

Never hesitate to visit an emergency room for these life-threatening conditions. Your life is worth infinitely more than any bill.

Go to ER immediately for:

Cardiovascular symptoms:

- Chest pain or pressure

- Pain radiating to arm, jaw, or back

- Severe shortness of breath

- Irregular or rapid heartbeat with dizziness

Neurological symptoms:

- Sudden weakness or numbness on one side of body

- Difficulty speaking or understanding speech

- Sudden severe headache (“worst headache of my life”)

- Vision changes in one or both eyes

- Loss of consciousness

- Seizures (especially first-time)

- Confusion or altered mental status

Trauma:

- Major injuries from car accidents, falls, or violence

- Head injuries with loss of consciousness

- Severe bleeding that won’t stop

- Deep wounds or large cuts

- Suspected broken bones (especially long bones or spine)

- Severe burns (over 10% of body, face, hands, feet, or genitals)

Respiratory emergencies:

- Severe difficulty breathing

- Choking

- Inability to speak in full sentences due to breathing difficulty

Other true emergencies:

- Severe allergic reactions (anaphylaxis)

- Coughing or vomiting blood

- Severe abdominal pain (especially if pregnant)

- Poisoning or drug overdose

- Suicidal or homicidal thoughts with intent

- High fever with stiff neck or altered mental status

- Sudden severe pain anywhere

When in doubt about whether symptoms are life-threatening, always choose the ER. False alarms cost money but save lives.

When Urgent Care Is the Better Choice

Urgent care centers handle non-life-threatening conditions that need same-day attention but aren’t emergencies. Here’s what they treat effectively:

Perfect for urgent care:

Infections:

- Urinary tract infections

- Ear infections

- Sinus infections

- Strep throat

- Pink eye (conjunctivitis)

- Skin infections

Minor injuries:

- Sprains and strains

- Minor cuts requiring stitches (under 2 inches, not deep)

- Minor burns (1st or 2nd degree, small area)

- Minor fractures (fingers, toes)

- Insect bites and stings

- Minor animal bites

Respiratory issues:

- Cough and cold symptoms

- Flu symptoms

- Mild asthma attacks (if you can speak in full sentences)

- Bronchitis

Digestive issues:

- Vomiting or diarrhea without severe dehydration

- Mild to moderate abdominal pain

- Food poisoning

Skin conditions:

- Rashes

- Mild allergic reactions (no breathing difficulty)

- Minor skin abscess

Other conditions:

- Fever (without severe symptoms)

- Back pain (without neurological symptoms)

- Minor eye injuries (no penetrating trauma)

- Mild dehydration

- Simple STI testing

Finding Urgent Care in New York

New York, particularly NYC, has extensive urgent care coverage with over 200 centers across the five boroughs and hundreds more throughout the state.

Major urgent care chains in New York:

CityMD:

- 140+ locations across NYC, Long Island, Westchester

- Open 365 days/year, 8am-8pm (most locations)

- Accepts most insurance plans

- Walk-in and online check-in available

- Average cost: $150-$250 without insurance

Northwell Health-GoHealth Urgent Care:

- 40+ locations in NYC and Long Island

- Extended hours including weekends

- Part of Northwell Health system

- Seamless referrals if you need ER

PM Pediatrics (for children):

- Pediatric-focused urgent care

- Multiple NYC locations

- Evening and weekend hours

- Board-certified pediatricians

Immediate Care Centers (various providers):

- Community urgent care centers throughout NYS

- Often more affordable than chains

- Check if they accept your insurance

How to find nearby urgent care:

- Search “urgent care near me” on Google Maps

- Check your insurance app/website for in-network facilities

- Call ahead to confirm hours and insurance acceptance

- Use online check-in to reduce wait time

Decision-Making Framework

Still unsure where to go? Use this simple decision tree:

Is this a potential emergency? (chest pain, severe bleeding, difficulty breathing, stroke symptoms, severe trauma) → GO TO ER IMMEDIATELY

Are you experiencing moderate symptoms that need care today but aren’t life-threatening? (UTI, sprained ankle, minor cut, ear infection) → TRY URGENT CARE FIRST

- If urgent care is closed: ER

- If urgent care can’t handle your condition: They’ll direct you to ER

Can you wait 1-2 days for an appointment? (routine illness, chronic condition management, preventive care) → CALL YOUR PRIMARY CARE DOCTOR

Need medical advice but no physical exam required? (medication questions, minor symptoms, general health questions) → TRY TELEHEALTH

Still not sure? → Call your insurance company’s 24/7 nurse line (number on your insurance card)

Most insurance plans offer free 24/7 nurse hotlines where registered nurses help you determine appropriate care setting. They’ll ask about symptoms and advise whether you need an ER, urgent care, or can wait for your doctor.

Other Lower-Cost Alternatives to Consider

Community Health Centers (Federally Qualified Health Centers – FQHCs):

- Sliding scale fees based on income

- Comprehensive services including urgent care

- Many open evenings and weekends

- Found throughout NYC and NY State

- Search: findahealthcenter.hrsa.gov

Retail Clinics:

- Located in CVS, Walgreens, Rite Aid pharmacies

- Treat minor conditions (colds, flu, vaccines, minor skin conditions)

- Cost: $60-$125 per visit

- Very limited scope compared to urgent care

- No appointments needed

Telehealth Services:

- Available through most insurance plans

- Direct-to-consumer options (Teladoc, MDLive, Doctor on Demand)

- Cost: $40-$75 without insurance, often $0-$20 copay with insurance

- Available 24/7

- Can prescribe medications

- Good for: flu, UTI, rashes, pink eye, minor issues

- Cannot do physical exams or diagnostic tests

NYC Health + Hospitals ExpressCare:

- Virtual urgent care for NYC residents

- Free or low-cost based on insurance/income

- Available daily 8am-midnight

- Access via app or website

10 Proven Ways to Reduce Your Emergency Room Bill in New York

Even after receiving an ER bill, you have significant power to reduce what you actually pay. These strategies have helped thousands of New Yorkers save 50-90% on their emergency room costs.

1. Request an Itemized Bill Immediately

Studies show that up to 80% of medical bills contain errors. An itemized bill reveals exactly what you’re being charged for and makes errors visible.

How to request:

- Call hospital billing department

- Ask for: “A detailed, itemized bill with CPT codes and service descriptions”

- Federal law requires they provide this

- Request within 30 days of receiving summary bill

What to look for:

- Duplicate charges (same service billed twice)

- Services you didn’t receive

- Incorrect quantities (billed for 3 X-rays when you had 1)

- Unbundled charges (separate billing for services that should be bundled)

- Upcoded services (billed for higher complexity than received)

Common errors in ER bills:

- Operating room charges (when only ER was used)

- Discharge planning fees (for simple ER visits)

- Supplies charged individually that should be in facility fee

- Incorrect emergency level code

Real example: Brooklyn patient received $4,200 ER bill for chest pain. Itemized bill revealed:

- Duplicate charge for cardiac monitoring: $600

- Two EKGs billed, only one performed: $200

- Level 2 ER visit coded as Level 1: $400 difference Errors totaled: $800 (19% of bill)

After disputing errors, bill reduced to $3,400. Then applied for financial assistance, final responsibility: $0.

2. Challenge Charges You Don’t Understand

Don’t pay for anything you can’t verify or don’t understand.

Questions to ask billing department:

- “What is CPT code [number] and when was this service provided?”

- “Why am I being charged for [specific item]?”

- “Can you explain the difference between the facility fee and physician fee?”

- “Are these charges at Medicare rates or chargemaster rates?”

Compare to Medicare rates: Medicare publishes what it pays for services. If your charge is 300-400% of the Medicare rate, it’s likely inflated. Use this as negotiation leverage.

Challenge these common questionable charges:

- Facility fees for services that should be bundled

- “Trauma activation” fees (if you weren’t a trauma patient)

- Separate charges for basic supplies (gloves, bandages)

- Consultation fees for specialists who didn’t actually consult

3. Apply for Financial Assistance (Even If You Think You Won’t Qualify)

This is the single most powerful strategy. Many New Yorkers who think they earn “too much” actually qualify.

Why you might qualify even with decent income:

- Income limits often extend to 300-400% of federal poverty level

- That’s up to $60,000 for an individual, $120,000 for a family of 4 at some hospitals

- Extraordinary medical expenses count

- Recent job loss or income reduction matters

- Household size includes dependents

Application process:

- Contact hospital financial counseling within 30 days of bill

- Ask specifically about “financial assistance policy” and “charity care”

- Request application (must be provided in your language)

- Gather documentation: pay stubs, tax returns, proof of expenses

- Submit application with all required documents

- Follow up weekly on status

- Appeal if denied (many denials are reversed on appeal)

What happens to your bill while applying:

- Collections must pause

- Credit reporting prohibited for up to 2 years in NY

- Payment deadlines extended

- Interest typically frozen

Approval timelines:

- Most hospitals respond within 30-45 days

- Complex cases may take 60-90 days

- You can apply up to 2 years after service

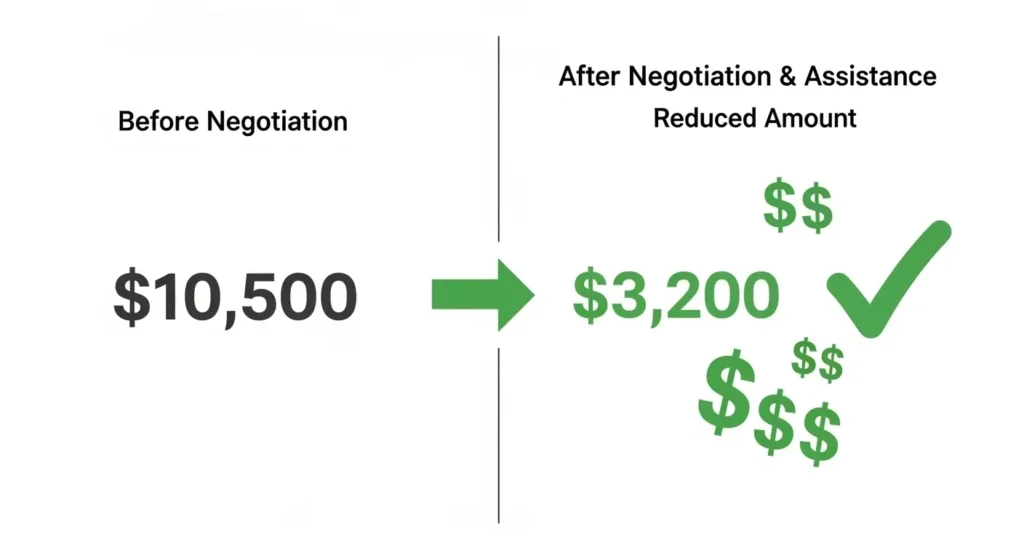

4. Negotiate Your Bill Directly

Medical bills are negotiable, especially for self-pay patients. Hospitals would rather receive partial payment than send bills to collections.

Negotiation strategies:

Start with a reasonable offer:

- For bills under $2,000: Offer 30-40% of billed amount

- For bills $2,000-$10,000: Offer 25-35%

- For bills over $10,000: Offer 20-30%

Justification points to use:

- “I’m self-pay and this is what I can afford”

- “This charge is [X]% higher than Medicare rates for the same service”

- “I found these billing errors [list them]”

- “I can pay [amount] today if you’ll settle in full”

Get everything in writing:

- Settlement amount

- “Paid in full” language

- Deadline for payment

- Confirmation no remaining balance

Real negotiation example: Staten Island patient with $6,800 ER bill for broken arm (no surgery):

- Requested itemized bill: Found $400 in errors

- Adjusted bill: $6,400

- Made offer: $2,000 (31% of adjusted bill) if paid within 30 days

- Hospital countered: $3,200 (50%)

- Final settlement: $2,500 (39% of original bill)

- Total savings: $4,300 (63%)

5. Request Self-Pay Discounts

Many hospitals automatically offer discounts to uninsured patients who pay quickly.

Typical discount structures:

- 20-30% if paid within 30 days

- 15-20% if paid within 60 days

- Additional 5-10% for payment in full vs. payment plan

How to request:

- Ask at registration: “What self-pay discounts do you offer?”

- Request written policy

- Confirm discount percentage and deadline

- Get agreement in writing before paying

Can be combined with:

- Billing error corrections

- Further negotiation

- Financial assistance (sometimes)

6. Set Up an Interest-Free Payment Plan

If you can’t pay the full amount or negotiated settlement, payment plans prevent collections and credit damage.

Standard payment plan terms:

- No interest charges

- No credit check

- Minimum payments: $25-$100/month

- Duration: 12-36 months (some extend to 48-60 months)

How to maximize payment plan benefits:

- Propose lowest monthly payment you can reliably make

- Set up automatic payments (reduces missed payment risk)

- Pay extra when possible to reduce principal

- Keep all payment records

- Request confirmation when paid in full

Payment plan protects you:

- Prevents collection agency involvement

- Stops credit reporting

- Avoids legal action

- Maintains your credit score

Important: Even $25/month shows good faith and typically prevents collections. A $3,000 bill paid at $50/month takes 60 months but preserves your credit.

7. Use Medical Bill Advocacy Services

Professional advocates review bills, identify errors, and negotiate on your behalf.

Free or low-cost options:

Dollar For (Non-Profit):

- Website: dollarfor.org

- Free service for low-income individuals

- Reviews bills and negotiates

- Success rate: ~70% achieve reduction

Patient Advocate Foundation:

- Website: patientadvocate.org

- Free case management

- Helps with financial assistance applications

- Mediates billing disputes

For-profit medical billing advocates:

- Charge 20-35% of amount saved

- Only pay if they reduce your bill

- Handle all negotiations

- Good for complex or very large bills

When to use advocates:

- Bills over $5,000

- Multiple billing errors

- Insurance claim denials

- Complex cases with multiple providers

- You’re overwhelmed by the process

8. Appeal Insurance Denials

If your insurance denies coverage for ER services, you have the right to appeal.

Common denial reasons:

- “Not medically necessary”

- “Should have gone to urgent care”

- “Non-emergency condition”

New York’s “prudent layperson” standard: Your insurance must cover ER visits if a reasonable person would believe the symptoms required emergency care—regardless of final diagnosis.

Example: Severe chest pain turns out to be indigestion. Insurance must still cover because chest pain reasonably suggests possible heart attack to a non-medical person.

Appeal process:

- Request written denial reason

- Get medical records from ER visit

- Write appeal explaining why symptoms warranted ER care

- Include physician statement supporting medical necessity

- Submit within timeframe specified in denial letter (typically 30-180 days)

- Escalate to external review if internal appeal denied

New York appeal rights:

- Internal appeal to insurance company

- External appeal to independent reviewer

- File complaint with NY Department of Financial Services

9. Check for Billing Code Errors

Medical billing uses standardized CPT (procedure) and ICD-10 (diagnosis) codes. Incorrect codes can dramatically inflate charges.

Common coding errors:

Upcoding:

- Billed as Level 1 ER visit (most severe) when you had Level 3 (moderate)

- Simple procedure coded as complex

- Higher code used than medical record supports

Unbundling:

- Charging separately for services that should be billed together

- Example: Billing for individual IV supplies when they should be included in IV therapy code

Wrong codes:

- Copy-paste errors from previous patients

- Administrative mistakes

- Deliberate overbilling

How to check:

- Get itemized bill with all CPT codes

- Look up codes: www.aapc.com or www.cms.gov

- Compare codes to actual services received

- Check medical record matches billed codes

- Challenge discrepancies with billing department

10. Know When to Get Legal Help

For very large bills or when hospitals refuse reasonable resolution, consider legal assistance.

When to consult an attorney:

- Bills over $25,000 with no financial assistance approval

- Hospital threatens lawsuit

- Wages being garnished

- Believe you’re victim of fraudulent billing

- Discrimination in financial assistance application

Free legal resources in New York:

- Legal Aid Society: legal-aid.org

- New York Legal Assistance Group: nylag.org

- Empire Justice Center: empirejustice.org

- LawHelpNY.org: Find local legal aid

Consumer protection laws: New York has strong consumer protection laws regarding medical billing. Attorneys can help if hospitals violate:

- Fair debt collection practices

- Financial assistance law requirements

- Billing transparency rules

- Patient rights protections

Understanding Your ER Bill: What You’re Actually Paying For

The emergency room cost in New York isn’t one simple charge. Understanding the components helps you identify errors and negotiate effectively.

Facility Fee (Emergency Department Charge)

This is typically the largest component of your ER bill—the charge for using the emergency department itself.

What it covers:

- Use of ER space and equipment

- Nursing care

- Medical supplies (basic)

- Overhead costs (24/7 staffing, maintaining ER)

- Administrative services

Typical range in New York: $250-$4,500 depending on visit level

Coded as: CPT codes 99281-99285

- 99281 (Level 5): Minor, self-limited problem ($250-$600)

- 99282 (Level 4): Low to moderate severity ($400-$900)

- 99283 (Level 3): Moderate severity ($700-$1,500) — Most common

- 99284 (Level 2): High severity ($900-$2,500)

- 99285 (Level 1): Life-threatening ($1,200-$4,500)

The level assigned depends on:

- Severity of presenting symptoms

- Number of body systems examined

- Complexity of medical decision-making

- Amount of physician time required

Physician/Provider Fees

Emergency physicians typically bill separately from the hospital facility. You’ll receive two bills for one ER visit.

Professional services billed separately:

- Emergency physician evaluation and management

- Procedures performed by physicians

- Specialist consultations

Typical range in New York: $200-$1,500 depending on complexity

Why separate billing: Many emergency physicians are contracted independent providers, not hospital employees. This is why surprise billing was such a problem before legal protections.

Under current law: You pay only in-network rates for emergency physician services, even if the physician is out-of-network.

Laboratory Services

Each lab test is billed individually with separate professional (pathologist reading) and technical (running the test) components.

Common ER lab tests and typical costs:

- Complete Blood Count (CBC): $50-$150

- Basic Metabolic Panel: $50-$150

- Comprehensive Metabolic Panel: $75-$200

- Urinalysis: $30-$100

- Pregnancy test (urine): $30-$80

- Cardiac enzymes (troponin): $100-$300

- Blood alcohol level: $50-$150

- Drug screening: $100-$300

- Cultures (blood, urine, throat): $100-$400 each

Each test billed separately: If you had 5 different blood tests, expect 5 separate lab charges.

Radiology/Imaging

Imaging studies are often the most expensive component of ER bills.

Typical costs for common imaging:

- Single X-ray view: $100-$300

- Multiple X-ray views (2-3): $200-$600

- CT scan (head, abdomen, chest): $500-$3,000

- MRI: $1,000-$5,000

- Ultrasound: $300-$1,000

Billed in two parts:

- Technical component: Equipment use, technician

- Professional component: Radiologist interpretation

Why CT scans are expensive:

- Advanced equipment costs

- Radiologist expertise

- Image processing and storage

- May be billed with and without contrast (two separate charges)

Medications and Treatments

Medications administered in the ER are billed separately and often marked up significantly from retail pharmacy prices.

Common medications and costs:

- IV antibiotics: $200-$500 per dose

- Pain medications (injected): $50-$200

- Nausea medications: $50-$150

- IV fluids (saline): $100-$400

- Nebulizer treatments: $100-$300

- Oral medications: $20-$100

Why ER medications cost more:

- Immediate availability 24/7

- IV administration complexity

- Pharmaceutical stocking costs

- Regulatory compliance costs

Medical Supplies

Every supply item can be billed separately:

- Splints and braces: $50-$300

- Crutches: $50-$150

- Casting materials: $100-$500

- Suture kits: $100-$400

- Bandages and dressing materials: $20-$150

- IV supplies (catheters, tubing): $50-$200

- Oxygen delivery: $50-$300

Procedures

Specific procedures have their own codes and charges:

- Laceration repair (stitches): $200-$1,000 depending on complexity

- Splinting or casting: $100-$500

- Incision and drainage (abscess): $200-$800

- Foreign body removal: $200-$600

- Wound debridement: $300-$1,200

Timeline: When to Expect Bills

ER billing doesn’t happen all at once. Expect multiple bills arriving over 2-3 months:

Week 1-2 after visit:

- Facility bill (hospital ER charge) often arrives first

Week 3-6:

- Emergency physician bill

- Laboratory bills (may be separate from facility)

Week 4-10:

- Radiology/imaging professional fees

- Specialist consultation bills (if any)

- Ambulance bill (if separate company)

Week 8-12:

- Straggler bills from various providers

- Corrected or adjusted bills

Don’t panic if bills trickle in. This is normal. Keep all bills together and note they’re for the same visit when reviewing or applying for financial assistance.

Reading Your Bill: Key Terms

Chargemaster price: The hospital’s list price before any discounts Allowed amount: What insurance agrees to pay (negotiated rate) Patient responsibility: What you owe after insurance Copay: Fixed amount you pay (e.g., $250) Coinsurance: Percentage you pay (e.g., 20% of allowed amount) Deductible: Amount you must pay before insurance coverage kicks in Out-of-pocket maximum: Most you’ll pay in a year Balance billing: Charging you the difference between provider’s charge and insurance payment (illegal for emergency services in NY) Adjustment: Reduction in charges (insurance discount, financial assistance, error correction)

Understanding these components empowers you to question charges, identify errors, and negotiate from an informed position.

Your Rights as an ER Patient in New York

New York provides some of the nation’s strongest patient protections. Knowing your rights helps you avoid unfair charges and access the care you need.

Right to Emergency Care Regardless of Ability to Pay (EMTALA)

The federal Emergency Medical Treatment and Labor Act (EMTALA) guarantees emergency care rights:

Hospitals must:

- Provide medical screening examination to anyone requesting emergency care

- Stabilize any emergency medical condition before discharge or transfer

- Not inquire about ability to pay before providing stabilizing treatment

- Not transfer unstable patients to other facilities

You cannot be:

- Turned away due to inability to pay

- Asked to pay before receiving emergency treatment

- Transferred while medically unstable

- Required to provide insurance information before being seen (though registration will ask)

Violations to report:

- Being told to go elsewhere due to lack of insurance

- Delayed treatment while insurance verification occurs

- Transfer request before medical stabilization

- Discharge while emergency condition persists

How to report EMTALA violations:

- Centers for Medicare & Medicaid Services (CMS): 1-800-MEDICARE

- New York State Department of Health: 1-800-804-5447

No Surprises Act: Federal Protection Against Balance Billing

Effective January 1, 2022, the No Surprises Act provides comprehensive protection against unexpected medical bills.

Key protections for emergency services:

You cannot be balance-billed for:

- Emergency services at out-of-network facilities

- Emergency services from out-of-network providers

- Out-of-network ground ambulance services

Your cost-sharing (copay, coinsurance, deductible) must be:

- Calculated at in-network rates

- Applied to in-network out-of-pocket maximums

- No higher than if you’d received care in-network

Providers cannot:

- Ask you to waive your balance billing protections

- Bill you the difference between their charge and insurance payment

- Require you to sign forms waiving these protections

Good faith estimates:

- Uninsured/self-pay patients can request cost estimates

- Must be provided within 3 business days

- Helps you plan for expenses

- If final bill is $400+ higher than estimate, you can dispute

Dispute resolution:

- If you receive improper balance bill, don’t pay

- Contact your insurance immediately

- File complaint with federal agencies

- Use IDR (Independent Dispute Resolution) process

New York’s Surprise Billing Protections

New York State had surprise billing protections before the federal No Surprises Act, and some provisions remain stronger.

New York’s protections include:

- Coverage for emergency services at in-network rates regardless of network status

- Independent Dispute Resolution process for billing disputes

- Prohibition on balance billing for most surprise bills

- Consumer assignment of benefits to resolve disputes without patient involvement

How NY’s IDR process works:

- Provider and insurer attempt to negotiate payment

- If no agreement within 30 days, either party can request IDR

- Independent arbitrator decides payment amount

- Patient never involved in the dispute

- Patient pays only in-network cost-sharing

Financial Assistance Rights Under New York Law

New York’s Financial Assistance Law (FAL) creates powerful consumer protections:

Hospitals must:

- Post financial assistance policies publicly (in English and other common languages)

- Screen patients for eligibility during registration and billing

- Provide applications in multiple languages

- Process applications within reasonable timeframes

- Provide written decision with appeal rights

Patients have the right to:

- Apply for financial assistance up to 2 years after service

- Receive application in their language

- Appeal denials with additional documentation

- Protection from credit reporting while application pending (up to 2 years)

- Written explanation if denied

Hospitals cannot:

- Report to credit agencies for 2 years after service if FAL application is pending

- Commence collection actions before reviewing FAL application

- Deny emergency care while discussing financial assistance

Eligibility considerations:

- Household income relative to Federal Poverty Level

- Household size including dependents

- Available assets (varies by hospital)

- Extraordinary medical expenses

Patient Bill of Rights in New York

New York law guarantees comprehensive patient rights:

Right to information:

- Full explanation of diagnosis, treatment options, and risks

- Access to your medical records within reasonable time

- Understandable information about costs before elective procedures

Right to make decisions:

- Accept or refuse treatment (with rare exceptions)

- Consent to treatment in language you understand

- Designate healthcare proxy

Right to privacy:

- HIPAA protections for medical information

- Confidential treatment of records

- Consent required before information sharing (with specific exceptions)

Right to language services:

- Free interpretation services if you don’t speak English

- Translated consent forms and key documents

- No requirement to use family members as interpreters

Right to respectful care:

- Treatment without discrimination

- Cultural and religious considerations respected

- Accommodations for disabilities

How to File Complaints About Billing or Care

If you believe your rights have been violated or you’ve been unfairly billed:

Hospital Patient Advocate/Ombudsman (First Step):

- Every New York hospital has patient advocate

- Request meeting to discuss concerns

- Often resolves issues without formal complaint

- Document all conversations

New York State Department of Health:

- Phone: 1-800-804-5447

- Online: health.ny.gov (complaint portal)

- Investigates billing complaints, quality of care issues

- Can result in corrective action against hospital

New York State Department of Financial Services:

- For insurance-related disputes

- Consumer hotline: 1-800-342-3736

- Online complaint form available

- Handles surprise billing complaints

Consumer Financial Protection Bureau (CFPB):

- For medical debt collection issues

- File online: consumerfinance.gov/complaint

- Monitors patterns of unfair debt collection

Attorney General’s Office:

- Health Care Bureau: 1-800-771-7755

- Handles fraud and abuse complaints

- Can investigate systematic billing problems

Statute of Limitations on Medical Debt in New York

Medical debt collection timeframe:

- 6 years from date of service or last payment

- After 6 years, debt is time-barred (uncollectible through lawsuit)

- Hospitals cannot sue for payment after statute expires

Financial assistance application window:

- 2 years from date of service under New York FAL

- Can apply even if bills are in collections

- If approved, previously paid amounts may be refunded

Credit reporting:

- Medical debt under $500 no longer reported by major credit bureaus

- Paid medical debt removed from credit reports

- Medical debt must be at least 1 year old before reporting (industry standard)

- New York FAL prohibits reporting while application pending (up to 2 years)

Protection From Aggressive Collection Practices

New York and federal law limit what debt collectors can do:

Collectors cannot:

- Call before 8am or after 9pm

- Contact you at work if you’ve asked them not to

- Harass, threaten, or abuse you

- Misrepresent amount owed or legal status

- Contact family/friends/employers about your debt (except to locate you)

- Add unauthorized fees or interest (medical debt is typically interest-free)

You have the right to:

- Request debt validation (proof you owe the debt)

- Dispute incorrect amounts

- Request collectors stop calling (must be in writing)

- Negotiate payment arrangements

- Apply for financial assistance even after collections begin

Fair Debt Collection Practices Act (FDCPA) violations: Report to:

- Consumer Financial Protection Bureau: consumerfinance.gov/complaint

- New York Attorney General: 1-800-771-7755

- Federal Trade Commission: ftc.gov/complaint

Understanding your rights transforms you from a passive recipient of bills into an empowered consumer who can navigate New York’s healthcare billing system effectively.

Special Situations: Emergency Room Costs in Unique Circumstances

Certain situations create unique considerations for emergency room costs in New York. Here’s what you need to know if you’re in special circumstances.

Ambulance Costs in New York

Ambulance transportation is typically billed separately from your ER visit, adding significant cost.

Average ambulance costs in New York:

- Basic Life Support (BLS): $500-$1,000

- Advanced Life Support (ALS): $800-$1,500

- Critical Care Transport: $1,500-$3,000+

- Mileage charges: $15-$50 per mile (added to base rate)

New York City EMS (911):

- NYC Fire Department operates 911 ambulances

- Generally lower cost than private ambulances

- Still billed to patients/insurance

- Financial assistance available

Private ambulance services:

- Typically more expensive

- Often out-of-network even when hospital is in-network

- Subject to surprise billing protections (ground ambulances only)

Insurance coverage:

- Most insurance covers emergency ambulance transport

- Copays typically $100-$500

- May require medical necessity documentation

- Non-emergency transport may not be covered

If you can’t afford ambulance bill:

- Apply for financial assistance separately from ER bill

- Request itemized bill and check for errors

- Negotiate payment amount

- Set up payment plan

When to call 911: Don’t let ambulance cost concerns delay calling 911 for true emergencies (chest pain, severe bleeding, difficulty breathing, stroke symptoms, unconsciousness).

Out-of-State Residents Visiting New York

If you experience a medical emergency while visiting New York:

Insurance coverage:

- Most insurance plans cover emergency care nationwide

- You’ll pay your standard copay/deductible

- Emergency services covered at in-network rates even if hospital is out-of-network (No Surprises Act)

What to do:

- Keep insurance card accessible while traveling

- Know your policy’s emergency coverage

- Call insurance company after ER visit to notify them

- Keep all receipts and medical records

If you’re uninsured:

- You’ll receive care regardless (EMTALA)

- Costs same as for New York residents

- Financial assistance typically requires New York residency (varies by hospital)

- Negotiate bill and request payment plan

Medicare coverage:

- Medicare covers emergency care anywhere in U.S.

- Pay standard Medicare cost-sharing

- Medicare Advantage plans cover emergency care out of service area

Medicaid:

- Emergency coverage varies by state

- Some states have reciprocal agreements

- Contact your state Medicaid office

Undocumented Immigrants and Emergency Care

New York provides strong protections for immigrants regardless of status.

Your rights:

- Cannot be denied emergency care due to immigration status

- EMTALA requires treatment for all emergency conditions

- No citizenship questions affect emergency care provision

- Immigration enforcement cannot occur in healthcare settings (sanctuary policies)

Emergency Medicaid:

- Covers emergency services for those ineligible for regular Medicaid only due to immigration status

- Includes ER visits, emergency surgery, dialysis, labor and delivery

- Apply at hospital or local Department of Social Services

- No immigration consequences for applying

NYC Health + Hospitals:

- Explicit policy: no one turned away due to immigration status

- Options program for uninsured regardless of status

- Confidentiality protections

- Interpretation services available

Financial assistance:

- Many hospital financial assistance programs available regardless of immigration status

- NYC Health + Hospitals doesn’t require citizenship/legal status

- Private hospitals vary – ask about eligibility

Privacy protections:

- Healthcare providers cannot share immigration status information with ICE

- Medical records are protected under HIPAA

- Hospital staff are not immigration enforcement agents

What to know:

- Bring any available ID (doesn’t need to be government-issued)

- Provide emergency contact information

- Ask about financial assistance in your language

- Don’t let fear prevent seeking emergency care

Pregnancy-Related Emergency Room Visits

Pregnancy emergencies have unique coverage considerations:

Common pregnancy-related ER visits:

- Severe abdominal pain

- Vaginal bleeding

- Severe headache with vision changes (preeclampsia)

- Decreased fetal movement

- Labor and delivery

- Pregnancy complications

Insurance coverage:

- Emergency pregnancy care covered by all insurance plans

- Maternity coverage included in all ACA-compliant plans

- Medicaid covers pregnant women at higher income levels (up to 218% FPL in NY)

- Emergency Medicaid covers labor and delivery regardless of immigration status

Presumptive eligibility:

- Pregnant women can receive temporary Medicaid approval same day

- Covers pregnancy-related emergency care immediately

- Full application processed later

- Available at many hospitals and clinics

Labor and delivery in ER:

- If you deliver in ER (before transfer to L&D), billed as ER visit plus delivery

- Can be more expensive than planned delivery

- Usually covered same as standard delivery under insurance

Uninsured pregnant women:

- Medicaid expansion covers more pregnant women

- NYC Health + Hospitals provides prenatal and delivery care on sliding scale

- Emergency delivery cannot be denied due to ability to pay

Mental Health and Psychiatric Emergencies

Mental health crises warrant emergency care just like physical emergencies:

When to go to ER for mental health:

- Suicidal thoughts with intent or plan

- Homicidal thoughts

- Severe psychotic symptoms

- Inability to care for yourself

- Dangerous behavior

Costs:

- Psychiatric emergency evaluation: Similar to medical ER visit

- Crisis stabilization: $1,000-$5,000 per day

- Inpatient psychiatric admission: $1,000-$3,000 per day

Insurance coverage:

- Mental health parity laws require equal coverage

- Cannot have higher copays for psychiatric ER vs. medical ER

- Inpatient psychiatric care covered like medical hospitalization

Lower-cost alternatives for non-emergency mental health:

- NYC Well: 1-888-NYC-WELL – Free confidential mental health support 24/7

- Mobile Crisis Teams: Come to you, often avoid ER

- Crisis Respite Centers: Short-term stabilization, less expensive than ER

- Community mental health centers: Sliding scale fees

Rights during psychiatric emergency:

- Cannot be held against your will unless danger to self/others

- Right to refuse medication (with exceptions)

- Right to contact family/attorney

- Must receive least restrictive appropriate care

Pediatric Emergency Room Visits

Children’s emergency care has special considerations:

Pediatric ERs vs. General ERs:

- Children’s hospitals have pediatric specialists

- Often better equipped for kids

- Costs generally similar to adult ERs

- Shorter wait times at dedicated pediatric ERs

Major NYC pediatric ERs:

- NYC Health + Hospitals/Bellevue Pediatric ER

- NewYork-Presbyterian Morgan Stanley Children’s Hospital

- NYU Langone Hassenfeld Children’s Hospital

- Children’s Hospital at Montefiore

Insurance for children:

- Child Health Plus (CHIP): Low-cost insurance for children

- Higher income limits than adult Medicaid

- Emergency care fully covered

- No copays for most services

Common pediatric ER visits:

- High fever (especially under 3 months)

- Respiratory distress

- Severe allergic reactions

- Head injuries

- Fractures

- Ingestion of toxic substance

PM Pediatrics (Urgent Care for Children):

- Pediatric-focused urgent care

- Board-certified pediatricians

- Open evenings and weekends

- Cost: $150-$300 (much less than ER)

- Good alternative for non-life-threatening issues

Financial assistance for pediatric care:

- All hospital financial assistance programs cover children

- NYC Health + Hospitals especially generous for pediatric care

- Many hospitals have special pediatric charity programs

Essential Resources for Managing ER Costs in New York

Having the right resources at your fingertips can save you thousands of dollars and significant stress when dealing with emergency room costs in New York.

Finding Financial Assistance

NYC Health + Hospitals Financial Assistance:

- Website: nychhc.org/care-access

- Phone: 844-NYC-4NYC (844-692-4692)

- Services: Options program for uninsured, sliding scale fees, financial screening

- Eligibility: New York City residents regardless of immigration status

- Languages: Services available in 200+ languages

New York State of Health (Health Insurance Marketplace):

- Website: nystateofhealth.ny.gov

- Phone: 1-855-355-5777

- Services: Enroll in Medicaid, Child Health Plus, Essential Plan, private insurance

- Open Enrollment: November-January annually

- Special Enrollment: Qualifying life events (job loss, birth, marriage, etc.)

Emergency Medicaid:

- Apply at: Hospital financial counseling office or local Department of Social Services

- Covers: Emergency services for those ineligible for regular Medicaid due to immigration status

- Who qualifies: Anyone meeting income requirements experiencing emergency medical condition

Patient Access Network Foundation:

- Website: panfoundation.org

- Services: Assistance with copays and medical expenses

- Eligibility: Varies by program, generally moderate income

Price Transparency Tools

Fair Health Consumer:

- Website: fairhealthconsumer.org

- Free tool: Look up typical costs by ZIP code

- Coverage: Dental, medical, and hospital costs

- How to use: Enter procedure code or keyword, your ZIP, and insurance status

- Benefit: Compare what others paid for same services in your area